How Much Revenue Do I Need Before I Quit My Day Job?

🕐 Read Time 7 Minutes

Key Takeaways

Business revenue and take-home pay are different, and the gap is often larger than expected.

A single good month is not enough. Focus on sustained, consistent income to gauge readiness.

Leaving your job works best when your business supports your life without constant stress.

You’re not just replacing a paycheck. You’re replacing everything that came with it.

Your side hustle is picking up steam, and clients are coming in. You’re doing the math in your head and thinking, “I’m bringing in $4,000 a month, and my paycheck from my day job is $3,500. I’m close.”

In reality, you’re not quite there yet.

Understanding why is what separates entrepreneurs who make a smooth transition into self-employment from those who have to crawl back to a salaried job six months later.

Your business revenue is not your paycheck. Confusing the two is one of the most common mistakes people make before going out on their own. If you don’t separate them, it’s easy to overestimate how “ready” you are.

So, before you send that “I quit” email, let’s take a closer look at what your numbers really need to support.

Revenue ≠ Take-Home Pay

When you're employed, a lot happens behind the scenes that you never see. Your employer withholds taxes, pays half your Social Security and Medicare, covers a chunk of your health insurance, and gives you paid vacation.

When you go out on your own, every single one of those costs falls on you. This is where cash flow planning becomes essential — knowing not just what's coming in, but what's going out and when.

Self-Employment Tax Rate

The current self-employment tax rate alone is 15.3%. That covers both the employee and employer share of Social Security and Medicare. Add federal and state income taxes on top (which you'll now pay quarterly as estimated taxes). A good rule of thumb is to set aside 15-25% of your total revenue for taxes before you spend any of it.

In practical terms, that means your $4,000 take-home goal is already closer to $4,700-$5,300 before taxes are paid. But we’re not done yet.

The Cost of Health Insurance for the Self-Employed

Health insurance is one of the biggest shocks for people leaving traditional employment. On your employer's plan, you might be paying $150–$300 each month because your employer is subsidizing the rest. As a self-employed person, you pay the full premium.

Realistic monthly ranges for self-employed health coverage can be:

Individual coverage: $450-$600 or more per month, depending on age, location, and plan tier

Family coverage: $1200-$1,800+/month

High-deductible plan + HSA: $200–$400/month for individuals, but comes with higher out-of-pocket costs when used

There’s a silver lining — if you're self-employed, you can deduct 100% of your health insurance premiums from your taxable income, as long as you're not eligible for coverage through a spouse's employer plan. This doesn't erase the cost, but it does help.

Other Expenses That Come Out of Revenue First

Even simple businesses have costs. Subscriptions, marketing, professional services, education, retirement savings, and equipment upgrades add up over time.

For many service-based businesses, expenses are 20-30% of revenue. If you assume 20%, then only 80 cents of every dollar you earn is left for pay and taxes.

If you need $4,000 per month for yourself, tack on another $800 in revenue to reach that goal.

Pay Yourself for Time Off

One of the biggest perks of a corporate job is Paid Time Off (PTO). When you're self-employed, if you don't work, you usually don't get paid. There’s no sick leave and no vacation days unless you account for that.

Build PTO into your revenue target. If you want three weeks of vacation plus a few sick days each year, that's roughly four weeks off. Plan to earn approximately four weeks' worth of extra revenue to give yourself sufficient breathing room for time off.

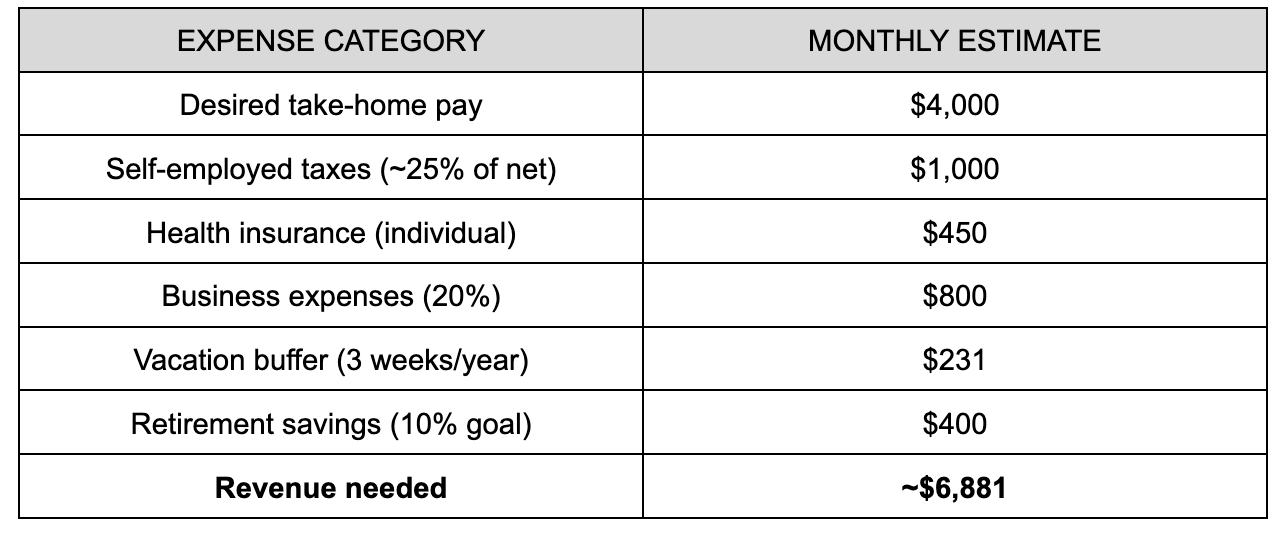

What Revenue Do I Really Need?

Let’s walk this through in a more practical way. If your goal is to take home $4,000 per month, there are several steps between that and the needed business revenue. The table below breaks down a realistic example of how these numbers add up.

Most people only see the top line. Cash flow planning is what helps you see the whole thing — and make a decision you won't regret six months later.

When you see it broken down this way, it's clearer why $4,000 in revenue isn't enough, and why building in these layers upfront makes the transition into self-employment more sustainable.

Not Everything Gets More Expensive

Up to this point, it might seem like everything’s getting more expensive. Some things are, but there’s another side that’s worth considering.

When you’re no longer commuting, buying work clothes, or grabbing convenience meals, your spending can shift in meaningful ways when you work for yourself.

If you have kids, the math can change even more. Flexible hours mean you might be able to skip paying for after-school childcare, catch a school event without burning PTO, or simply be around in ways that reduce the logistical expenses that pile up when two schedules don't align.

You may find yourself with more time to plan and more control over how you use your money. For some, this leads to lower expenses in areas that didn’t feel optional before.

Of course, this isn’t guaranteed. But it’s a reminder that your financial picture doesn’t exist in a vacuum — it’s connected to your daily life choices.

So, When Is the Right Time to Quit My Job?

Most people are looking for a moment — a specific number, or some kind of sign that says, “This is it.” But this decision can’t be based on one great month. It needs to focus on whether your business can consistently support your life.

Look at a stretch of at least six months, ideally closer to a year. If your income has been steady enough that a late invoice doesn't send you into a panic, that's a meaningful signal. It's the average that tells the real story, not the peaks.

If you’re waiting for a perfectly calculated, zero-risk moment to leave your job, you’ll probably wait forever. But that doesn’t mean you guess and hope for the best either. There isn’t one “right” path. Some people leave earlier and accept more uncertainty. Others wait until things feel almost boringly predictable. Both approaches can work as long as the decision is intentional.

When you can check off the list below without stretching the truth, you’re closer than you think:

3-6 months of living expenses saved as a cash cushion, separate from your business account.

Your full revenue target has been met consistently for at least 6 months. This should be based on average, not best-month revenue.

Health insurance plan identified and budgeted for.

An active pipeline of future work, not just current clients, but referral sources and prospects in the queue.

Quarterly estimated taxes set up and accounted for.

Business banking and account setup. Keep business and personal finances completely separate from day one.

A retirement savings plan in place — SEP IRA, Solo 401(k), Simple IRA, or a Traditional or Roth IRA

Being prepared enough to act without second-guessing is key.

Are You Ready to Determine Your Number?

Every situation is different. Your expenses, your income, and your timeline don’t fit neatly into a generic formula. That’s where we can help.

At Financial Fitness Coaching, we can help you sort through the numbers, test your plan, and create something that’s both realistic and sustainable without forcing you into a rigid system that does not fit your life.

If you’re wondering if you’re closer than you think, or what needs to change to get you there, let’s talk. Schedule a discovery call, and let’s turn that “someday” into a date on the calendar.

Frequently Asked Questions (FAQs)

Q: What expenses do people usually forget when going self-employed?

A: Health insurance, taxes, retirement savings, and paid time off are the big ones. These don’t show up in your business revenue, but you still need to fund them.

Q: What if my income is inconsistent month to month?

A: That’s normal for most business owners. Focus on your average income over several months and make sure you have a cash cushion for slower times.

Q: When should I quit my job and go full-time in my business?

A: There's no single magic number, but a few key signals point to readiness: your full revenue target has been met consistently for at least 6 months, you have 3–6 months of living expenses saved as a cash cushion, and you have a plan for health insurance, taxes, and retirement. If you can check those boxes without stretching the truth, you're closer than you think.

Q: What is cash flow planning, and why does it matter for new business owners?

A: Cash flow planning is tracking when money comes in and goes out of your business so you can make intentional decisions — including knowing exactly when you're ready to leave your day job.

Without it, it's easy to look at your revenue and feel ready when the full picture tells a different story. This is one of the core things we work on with clients at Financial Fitness Coaching.